John Taylor has a rather baffling article in the Wall Street Journal today where he doesn’t at all make the case against the Fed’s stimulus measures, though try as he might. Though he makes this claim that, given the premise, is easily checkable (and should be checked!):

At the very least, the policy creates a great deal of uncertainty. People recognize that the Fed will eventually have to reverse course. When the economy begins to heat up, the Fed will have to sell the assets it has been purchasing to prevent inflation.

If its asset sales are too slow, the bank reserves used to finance the original asset purchases pour out of the banks and into the economy. But if the asset sales are too fast or abrupt, they will drive bond prices down and interest rates up too much, causing a recession. Those who say that there is no problem with the Fed’s interest rate and asset purchases because inflation has not increased so far ignore such downsides.

So what does the market actually think about the balance of the risks?

From the yield curve, it looks like the market is fairly confident that the Fed can manage the unwinding of its current balance sheet. But why would the market think otherwise? In 2008, the Fed was given the authority to adjust an administered rate of interest on excess reserves. This is important, because normal monetary policy is about adjusting the monetary base in order to hit a market interest rate that the Fed is targeting. The Fed doesn’t control short term interest rates, but it coordinates expectations around it’s target by buying and selling assets. However, the IOER is a rate that the Fed has the ability to control directly (administer) and theoretically set at any rate it sees fit. This gives the Fed a high level of control over the unwinding of its balance sheet.

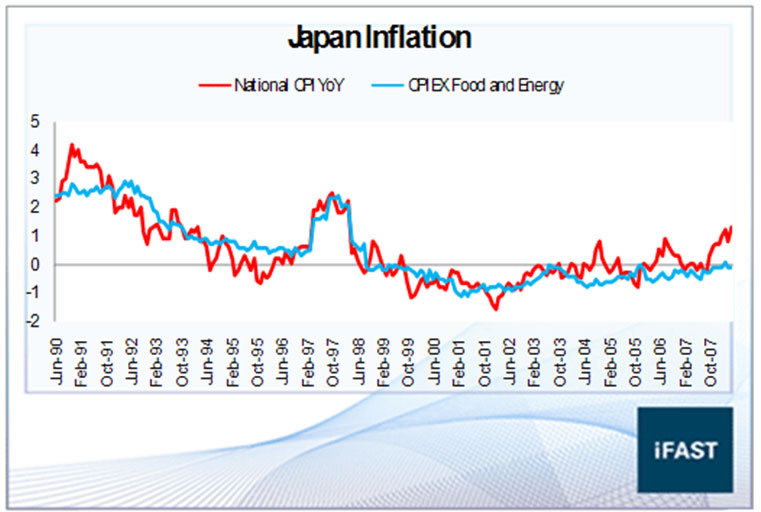

The entire yield curve is important here, because Taylor makes the claim that monetary stimulus advocates are ignoring the downside risks of inflation/recession given the Fed’s moves. Now it is theoretically possible that inflation expectations are characterized by tipping points, in which market indicators don’t move appreciably until enough “pressure” is built up that inflation snaps immediately to a new, dissimilar equilibrium (kind of like how fire sprinklers in an office building work, you’re either wet or dry depending on the precise temperature of mercury in the plug mechanism…no in between). However, it is instructive to look at the first case of quantitative easing asset purchases, and subsequent unwindings, to find evidence of this phenomenon. Japan doesn’t seem to provide any.

Furthermore, Taylor makes the extremely odd claim that forward guidance acts as a price ceiling on interest rates:

Consider the “forward guidance” policy of saying that the short-term rate will be near zero for several years into the future. The purpose of this guidance is to keep longer-term interest rates down and thus encourage more borrowing. A lower future short-term interest rate reduces long-term rates today because portfolio managers can, in a form of arbitrage, easily adjust their portfolio mix between long-term bonds and a sequence of short-term bonds.

[…]

[The Fed holding rates at zero] is much like the effect of a price ceiling in a rental market where landlords reduce the supply of rental housing. Here lenders supply less credit at the lower rate. The decline in credit availability reduces aggregate demand, which tends to increase unemployment, a classic unintended consequence of the policy.

This makes very little sense given the fact that the Fed is shifting demand for assets. By buying assets now, and promising to buy them in the future, the Fed is directly influencing the demand for the assets that it buys. Taylor is claiming that the Fed is providing a cap on returns on holding assets. Taylor’s analogy says that this policy is like the government mandating that everyone get a flu shot (would would cause shortages of flu shots), when the proper analogy would be that the government is providing inoculations in order to keep the price low.

Perversely, it is the lack of forward guidance that Taylor seems to be seeking that necessitated the moves in the Fed’s balance sheet that Taylor is now worried about. Had the Fed been providing forward guidance the whole time (for instance, a target for the level of NGDP), it is more likely that NGDP would have remained stable throughout this entire period, and that the Fed’s balance sheet would be a fraction of the size it is today, and presumably we would not be having this conversation.

Finally, Taylor makes this claim:

The Fed’s current zero interest-rate policy also creates incentives for otherwise risk-averse investors—retirees, pension funds—to take on questionable investments as they search for higher yields in an attempt to bolster their minuscule interest income.

This seems like it could make sense if you’re squinting, and given the controversial fact that a retirement fund has, indeed, begun trading in derivatives in order to escape the low return on fixed assets lends it credence…but lets not lose our sights here. Savers face a low rate of return on fixed assets because we just experienced the largest recession in postwar history, NGDP growth coming out has been sluggish and is projected to be sluggish into the future. Of course the Fed is to blame, but not in the way Taylor wants to.

Update: I don’t want to be unduly critical of everything Taylor says in this piece, as he does have some non-wacky points. For instance:

The low rates also make it possible for banks to roll over rather than write off bad loans, locking up unproductive assets.

and

More broadly, the Fed’s excursion into fiscal policy and credit allocation raises questions about its institutional independence and accountability. This reduces public confidence in the central bank.

{kind=link}

Niklas, welcome back!

Thanks, Marcus!

“[The Fed holding rates at zero] is much like the effect of a price ceiling in a rental market where landlords reduce the supply of rental housing. Here lenders supply less credit at the lower rate. The decline in credit availability reduces aggregate demand, which tends to increase unemployment, a classic unintended consequence of the policy.”–Taylor.

Okay, so the BoJ did QE from 2001-6, and Taylor gushes about it, in a paper you can find on his website.

The BoJ stopped QE (until recently) and still they had interest rates at ZLB. Indeed, sovereign yields globally are headed to ZLB.

Does Taylor really think the Fed can get out of ZLB by just raising interest rates?

On credit not being available due to low rates: Banks can raise rates to commercial bank customers (or homebuyers) if they wish and can charge higher rates–why does Taylor think they cannot? I would love to borrow at 0.25 percent and lend at 4 or 13 percent.

Moreover, A fed doing nothing policy—I guess the one advocated by Taylor—is often an activist policy, as in doing nothing when your dinner mate is choking and suffocating. An unintended consequence of doing nothing is that your dinner companion is asphyxiated. What makes helping your dinner partner activist vs. sitting and watching him/her die?

I realize I am conflating a few ideas here. i blame it on trying to understand Taylor’s reasoning. He strikes as a skilled boxer—now engaged in a bout with himself.

Is Taylor (and Goodhart) just short on bonds? I don’t get it.